Analysis: The challenge to build back better – as trust in insurance drops

Consumer trust in insurance has fallen over the past 12 months, but experts can see a route to a brighter future. Emmanuel Kenning reports.

Exclusive research for Insurance Age by Consumer Intelligence has revealed another fall in the public’s trust in the insurance industry.

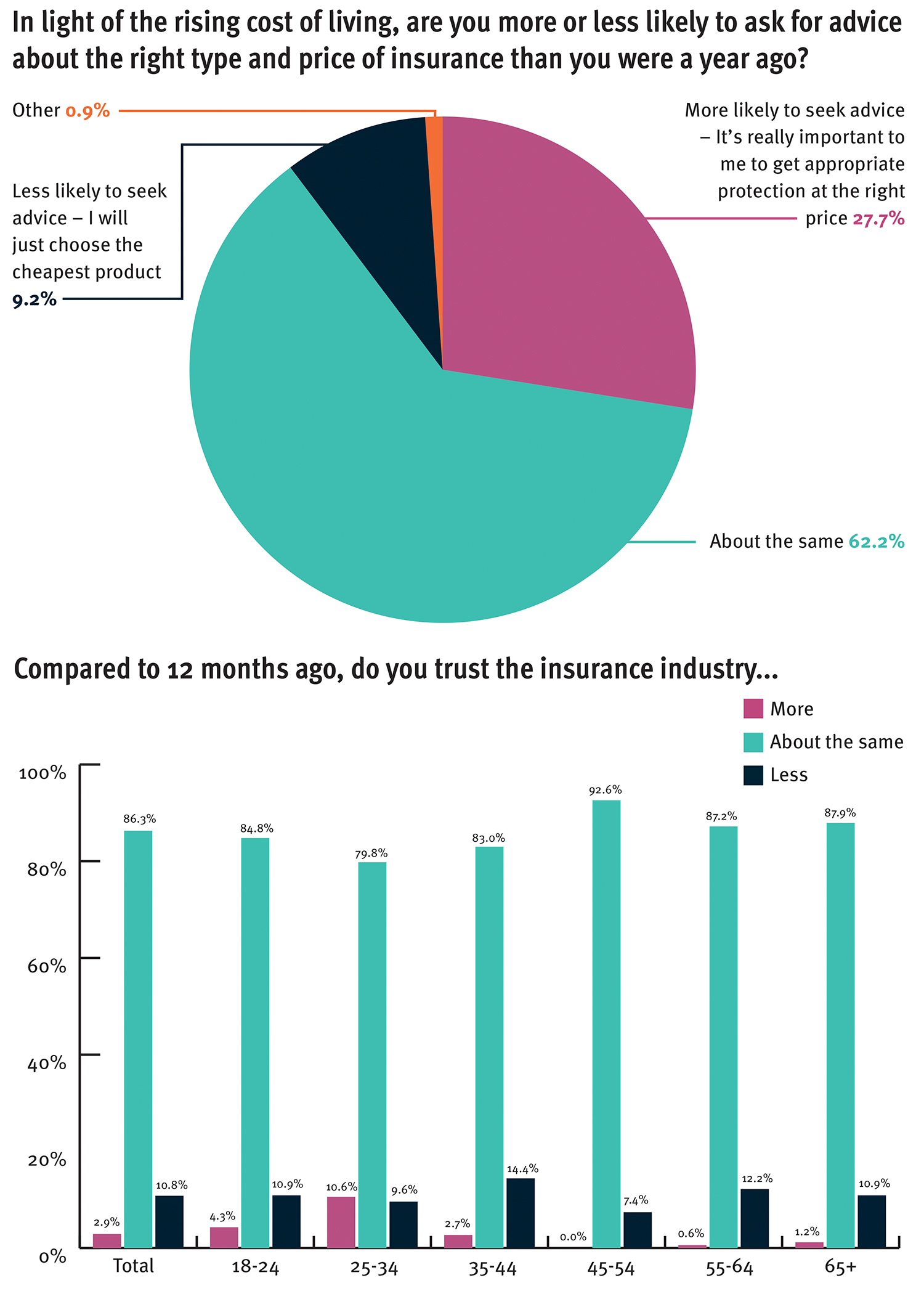

The survey asked 1055 adults about the change in their sentiment towards the sector over the past 12 months, and 11% detailed having less trust in the industry compared to 3% having more trust (see graph, below).

The age group with the biggest increase in positivity was the 25-34 year old bracket, where 11% of respondents reported enhanced trust. The cohort with the biggest increase in negativity was the 35-44 year olds – of which 14% said they had less trust in the industry.

Reputational damage

In June 2021, panellists at a Chartered Insurance Institute event urged brokers to tackle reputational damage, warning that the expectation gap between consumers and the industry had widened as a result of the Covid-19 pandemic.

Yet one year on, the evidence of the latest deterioration in the status of insurance among the public is revealed despite there arguably not having been as many negative headlines for the sector as compared with years gone by.

Stuart Reid, chairman of Partners& said he was saddened by the results of the survey, and highlighted that the impact of previous publicity around business interruption and challenges for people trying to claim on travel insurance for delays and cancellations due to Covid-19 had clearly continued.

“The industry has been in the cross hairs for the past few years,” he noted. “There has been an acknowledgement that the public does have an issue reputationally with insurers and brokers. It has been tough and that is no doubt reflected in the responses.”

Matthew Connell, director of policy and public affairs at the CII commented: “It is an important result and one we need to think about.”

In Connell’s opinion, the Financial Conduct Authority’s move on dual pricing will have a positive impact on trust in the long term, but at the moment the way the changes are unfolding are difficult for the public to interpret. Within the industry, it had been recognised that the rules would lead to price rises for some customers.

“If you are not one of the winners from that policy [dual pricing] it might have a short-term impact,” he stated.

In addition, inflation challenges for the industry and rising costs have meant price rises could have played a factor when the expectation was for falling premiums. Supply chain challenges have added to the expense and delayed repair times have hit the sentiment of policyholders making claims.

“The lesson is [to have] as much transparency as possible around why people are paying the premiums they are,” Connell observed.

According to the CII leader, over the past 12 months the industry has taken steps to restore its reputation.

“What brokers have done is move towards a more holistic model for advice,” he said, flagging that in the SME space uninsured risks were coming under the microscope and coverage was being better explained learning some of the lessons from the BI episode.

“There is a general move to deliver more information and give people help,” Connell continued.

Conversations with clients

Peter Blanc, CEO of Aston Lark, had been one of the experts on the CII panel and had called for improved conversations with clients.

“It is so tempting – as an insurance broker – to be like Father Christmas and just tell people what they want to hear, but actually our job is to tell people what they don’t want to hear sometimes. It is the right thing to do,” he updated.

Blanc’s view is that the industry has become a lot clearer – but it is clearer about what is not covered.

“I would say that we are being less ambiguous now,” he responded urging a move on to the next stage. “As an industry, we need to come up with solutions for the things that we currently don’t cover. It is not good enough just to say we don’t cover that. We need to find answers.”

Michael Lawrence, distribution and underwriting director for LV Broker, urged that good experiences for customers across communication and ease of dealing with the business, friendliness of staff, and how quickly and fairly claims are dealt with, are the key to turning around the reputation.

“Through your interaction with customers is where you will get the biggest impact in what you are trying to put across. Those good experiences are the ones that people will be able to share more,” Lawrence explained.

Adding: “You cannot go out and argue with the public. That is never really a good response. The way to do it is to show to the public this is what it is like when you are a customer of ours. That is the best way.”

Reasons to be optimistic

While insurance’s reputation has been knocked again over the past year, Consumer Intelligence’s findings uncovered several reasons for optimism. When asked about the cost of living crisis, 28% of the survey participants said it would make them more likely to seek advice, which is almost three times the amount who said they would be less likely and just seeking the cheapest quote (see chart, below).

Reid described this thirst for advice as news to celebrate, Blanc called it “incredibly good news” while Connell observed: “There is an audience out there who are willing to listen.”

The fact that price – while clearly a hygiene factor – is not the be all and end all was also well received. “Most people realise that there is no point in buying insurance at all if it is not giving you the right kind of protection and covering the right type of risks, and the insurer is not going to be there to pay out,” said Connell. “There is an appetite for knowing what the quality is as well as the price.”

Blanc stressed: “The lazy broker says my customer didn’t renew because they went elsewhere on price. It is almost never the case. Price is just one factor. It is about delivering and explaining that value.”

Insurance buying habits

The research also investigated the steps people will take when looking to make their next insurance purchase. Unsurprisingly, using an aggregator topped the responses. Reading online reviews came in second, which was cited by one-in-four people. Calling a provider to check an online quote is the most suitable for their needs rounded out the top three, with 19% of people saying they would do that.

More than half of the people planning to contact an insurance broker said they would use the telephone. However, the rise of technology was also clear, with 25% saying they would use a live chat offering. Buying in person (12%) and by email (11%) completed the findings.

Broker Igo4 has invested heavily in automation to drive efficiency in its business. CEO Matt Munro told Insurance Age that it had been “re-platforming” the customer experience over the last six years and was not surprised by this aspect of the survey results.

“It is all about convenience. It is how people want to manage their interactions. Over 97% of our customers quote and buy online. We are up to 70% of our customers being able to self-serve,” he revealed.

“That is not just about driving efficiencies in our operations, it is about how customers want to deal with us. If you have not got that digital platform you are not just missing out on a trick, you are not servicing customers in the way they want.”

Staying relevant

Lawrence also argued that staying relevant to customers was crucial, and advised: “Whether that is through face-to-face advice or a much more digital experience, you need to evolve your customer engagement – and do it well.

“It can be very damaging if you don’t get it right. Putting time into making sure that you can get an effective result for your customer is super important whatever way they choose to communicate with you.”

Reid concurred on live chat: “That aspect is something brokers are going to have to embrace – if they haven’t done so already. All forms of technology [and] any way we can communicate with our clients in a more efficient, friendly and instructive manner is a cause for celebration. Brokers ignore that at their peril.”

Meeting customers where they want to be met can only help support the rehabilitation of insurance’s reputation. But, ultimately, the sector needs to go further. Lawrence explained: “The message we need to get across in the industry is to live the experience and show people that we are highly reliable and deserve their trust because we earn their trust, and are going to continue to do so.”

Reid set out that striving for simplification in client interaction online and in person will do much to end the expectation gap, and help the sector’s standing in the eyes of the public.

“Sometimes, we fail to get across that the cover has its limitations before a claim occurs. The amount of paperwork, attachments and documents at each renewal, however well they are set up, is enough to put off any sane person. People aren’t reading their policy documents or synopsis of cover because there is so much to get through,” he said.

Connell concluded: “Consumers often do the research after their expectations haven’t been met rather than before. That is another challenge for the sector to think about how to design the customer journey to make sure these education points are brought through.

“It is not something we can shrug our shoulders about. It is something we have to crack one way or another.”

Overview

Ian Hughes, Consumer Intelligence CEO, analysed the survey findings, and commented: “As these results show, public trust in the insurance industry has fallen. One-in-10 people trust it less than they did a year ago, and only 3% trust it more.

“The reasons for that are complex, but include fallout from raised awareness of price walking – and the perception that claims aren’t being paid for Covid-19 pandemic-related travel interruption and business interruption.

“The results also demonstrate a clear public appetite for advice. Despite financial pressures, only a small minority of people – 9% – say they will just go for the cheapest possible policy next time around. Far more (28%) are crying out for extra support in choosing the right cover, and are influenced by recommendations, reviews and professional ratings.

“As many as one-in-five will call a provider to check what is covered after getting a quote from an online price comparison website.

“All this is an opportunity for brokers and direct insurers to articulate value from the outset. Providers need to make sure that they’re still on the other end of those telephones, especially for vulnerable customers, including older people and those [who are] experiencing financial instability.

“They need to be transparent about what is and what isn’t included in the policies, and develop clear pathways and options for those [who are] looking for help to get the appropriate protection at an appropriate price.”

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@insuranceage.co.uk.

You are currently unable to print this content. Please contact info@insuranceage.co.uk to find out more.

You are currently unable to copy this content. Please contact info@insuranceage.co.uk to find out more.

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Printing this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@insuranceage.co.uk

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Copying this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@insuranceage.co.uk

More on Insight

ERS and Acturis team up on full-cycle API car product for brokers

Acturis and specialist motor insurer ERS have launched an API based car insurance product for brokers on the software provider’s platform which replaces legacy EDI messaging.

People Moves: 30 May – 2 June 2023

Stay in the loop with the latest personnel moves in insurance.

Brokerbility adds A-One as member

A-One Insurance Group has joined Brokerbility, becoming the first member to sign up after the network unveiled a refreshed proposition in April.

Ardonagh expands into Greece

The Ardonagh Group has signed up to buy a majority stake in Athens-based SRS Group of Companies.

Jensten Group buys up Coversure member

The Jensten Group has bought the Coversure Poole Group for an undisclosed amount.

Interview: Melissa Collett

Melissa Collett left the CII at the end of May. A champion of professionalism and customer fairness, she has some wise words for an insurance industry on the brink of change.

US cannabis-focused MGU CannGen Insurance opens in Europe

North American managing general underwriter, CannGen Insurance Services, has launched a European operation citing an expectation that the continent’s legal cannabis market will grow quickly.

Verisk targets brokers and MGAs with Morning Data buy

Global data analytics and technology provider Verisk has bought Morning Data, a supplier of software to brokers and managing general agents in London and across the world.